Facebook (FB) reports quarterly earnings on January 30th. Analysts expect revenue of $16.4 billion and EPS of $2.19. The revenue estimate implies 26% growth Y/Y. Investors should focus on the following key items.

Stagnant MAU Growth

Facebook’s top line continues to show tremendous growth. I assumed that once its revenue got to a certain level that its growth would plateau. That moment has yet to arrive. Implied 26% revenue growth this quarter follows 33% growth in Q3. Operating income only grew 13% Y/Y as operating income margin fell to 42% from 50% in the year-earlier period. Facebook has increased investments in infrastructure, safety, and security in reaction to regulatory pressures. I find it difficult to believe the company cannot cut into these costs if revenue growth slows.

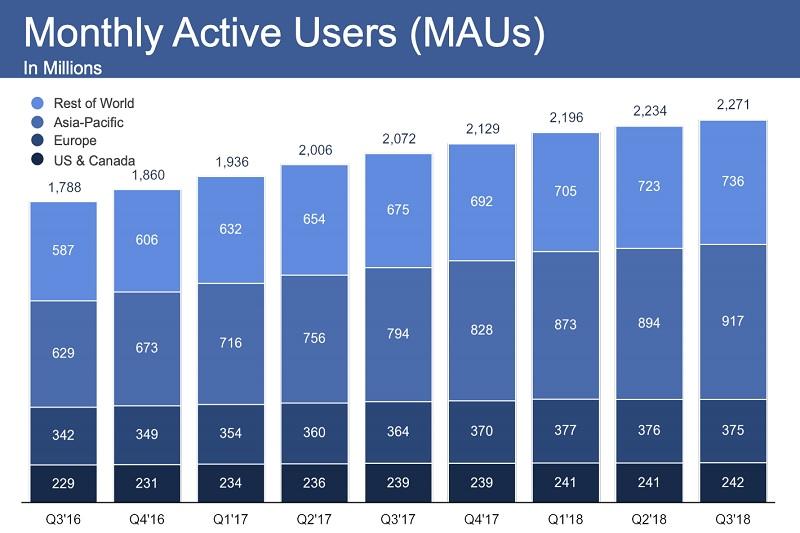

Monthly active users (“MAUs”) are already slowing. More than 2.6 billion people use Facebook, WhatsApp, Instagram, and Messenger each month, up from 2.5 billion in Q2 2018. This is a big selling point to advertisers; they can reach over 2 billion people with one advertising campaign. The question is, “How do you value that pool of users?”

MAUs were 2.3 billion at Q3 2018, up 10% Y/Y and 2% sequentially. As the chart illustrates, MAU growth appeared to have plateaued in Q4 2017. The days of double-digit sequential growth in MAUs are a thing of the past. MAUs could come under further scrutiny after PlainSite alleged a massive number of Facebook’s accounts are fake. Double-digit MAU growth is likely over. Read more:

{kind=link}

{kind=link}